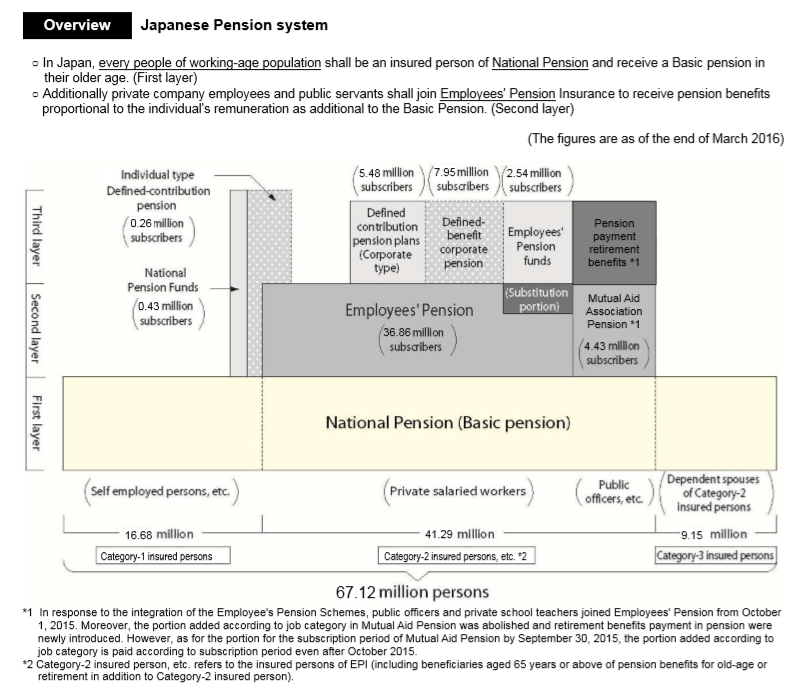

On top to mandatory public pension systems (National Pension, Employees Pension), there are optional pension systems for employees and individuals.

Among the optional pension systems, defined contribution pensions are attracting an increasing number of subscribers in recent years. Amount of pension benefit is determined by subscriber’s contribution and returns from investments in defined contribution pension system (often shortened as “DC”). DC pension is often compared against the other type, Defined Benefit (DB) pension, which pays to a pensioner a predefined amount of pension benefit. Like mandatory pensions, subscribers of optional pensions can also enjoy tax deduction. Some world talents in Japan subscribe a DC pension, especially when they work for a company which adopts corporate DC pension. There are mainly two types of DC pensions as follows.

- Corporate Type DC: Company contributes pension premium. An employee can add pension premium if so ruled.

- Individual Type DC (iDeCo): Individual subscriber contributes pension premium.

It should be noted that withdrawal is difficult until a subscriber reaches age 60. This restriction is intended to make sure DC pension fund being kept until then and used as income after retirement. (NB: DB pension however can be withdrawn e.g. when a subscriber changes job). More precisely, DC pension can be withdrawn when all of criteria below are satisfied, which is too stringent to be met for most of cases.

- Corporate Type DC – Criteria for withdrawal

- No longer participating any DC pension, neither corporate type nor individual type, as a subscriber or an investment instructor.

- Pension fund is not more than JPY 15,000.

- Still within 6 months since subscriber status of corporate type DC pension is lost.

- Individual Type (iDeCo) – Criteria for withdrawal

- Exempted from payment of National Pension Premium.

- Not entitled to receive disability benefits.

- Total subscription period is for not longer than 3 years, or Pension fund is not more than JPY 250,000.

- Still within 2 years since subscriber status of either corporate type or individual type DC pension is lost.

- Have not received lump sum withdrawal payment from corporate type DC pension.

As a case study, let us examine these criteria, for example, when a world talent leaves Japan after working in a company which has corporate type DC pension. If her/his pension fund is greater than JPY 15,000, which is quite likely, s/he cannot withdraw from the corporate DC pension. S/he then transfers the fund to an individual type DC pension (iDeCo), as s/he is no longer works for the company. However among the withdrawal criteria of the individual DC pension, the very first one, “Exempted from payment of National Pension Premium”, cannot be satisfied because s/he becomes out of scope of National Pension when s/he returns back to home country. Therefore, s/he cannot withdraw the fund even from the individual pension neither. S/he has to maintain the fund in the pension as an investment instructor until age 60. Only after reaching age 60, s/he can receive pension or lump sum payment.

The stringent criteria for withdrawal is however seen as a problem by Social Security Council of Japanese government, which proposes improvement through relaxation of the criteria as follows. So that this situation should be improved in the near future.

5 Withdrawal from DC Pension (Improvement in Lump Sum Payment)

– Lump-sum withdrawal should be made possible, when a foreigner returns back to home country, even for DC pension as for public pension systems.

– Because Non Japanese national can not subscribe iDeCo after leaving Japan, lump-sum withdrawal payment should be allowed, as long as other criteria are met, like pension subscription period being less than a certain duration.

– Lump-sum withdrawal should be allowed directly from corporate type DC pension, not requiring fund transfer to iDeCo, in order to streamline withdrawal procedures.

– The “not longer than 3 year” criterion, among criteria for withdrawal from individual DC pension, is set in line with withdrawal criteria for public pension. Now the criteria for public pension will be extended to 5 years, the DC pension criteria should be also extended to “not longer than 5 years” as well.

Source: Social Security Council – Corporate and Individual Pension Committee Minutes of Meeting on Dec 25th, 2019 (Translated by Anshin Immigration and Social Security Services)

Thank you for your reading this page. Should you have questions about withdrawal prior to or after returning back to home country, please contact the following for support:

- Corporate Type DC: HR department of your employer

- Individual Type (iDeCo): Financial institution you use for your iDeCo pension

Source: MHLW – Defined Contribution Pension – Overview (Japanese)